How can we quantify the potential equity portfolio losses that may be attributed to physical climate risk in the future? Over recent years, it has become increasingly important for pension funds and other investors to answer this question in ways that are credible, transparent, and in tune with regulators’ requirements. In this article (a summary of a recent paper[1]), we examine the European equity market using a ‘Climate Physical Loss (CPL)’ framework. The methodology is top-down, parsimonious, based on public data, and aligned with the NGFS scenario set[2]. Importantly, it is also directly applicable to asset allocation and portfolio construction due to its use of a discounted-cash-flow model and, therefore, of practical use to investors seeking not simply an assessment framework but a useable portfolio management tool.

This article explicitly focuses on European equities, while the following article (Quantifying Climate Physical Loss and Heterogeneity, Part 2: U.S. Equities) presents an application to U.S. listed equities.

Key takeaways

-

We find that European countries on average exhibit lower macroeconomic sensitivity to physical climate risks than the U.S., although there is a substantial amount of sector- and country-level heterogeneity, with larger projected deviations of nominal GDP in southern regions (e.g., -28% in Spain by 2100 under the NGFS ‘current policy’ scenario versus modest gains in Finland).

-

However, we find that the European cap-weighted equity benchmark displays a larger Climate Physical Loss (CPL) of -4.7%, versus -4.0% for the U.S benchmark.

-

This apparent dampening effect is primarily driven by benchmark composition, with the European equity market more exposed to low-WACC, higher-sensitivity sectors and more concentrated in physically vulnerable regions than its U.S. counterpart. As such, the research highlights the importance of portfolio construction in determining resilience.

Introduction: physical climate risk

Physical acute climate hazards such a s heatwaves, floods, droughts, storms and or chronic sea-level rise increasingly represent a challenge for firms and governments, as well as financially material risks for investors. Regulatory and supervisory authorities increasingly acknowledge that physical climate risks must be systematically integrated into risk management frameworks. The recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), followed by the issuance of the International Sustainability Standards Board’s IFRS S2 standard, have formalized the requirement to identify and disclose material physical and transition risks, underpinned by robust scenario analysis.

In Europe, regulatory and supervisory authorities have strongly acknowledged that climate-related risks may already be financially material and warrant forward-looking assessment. The European Central Bank’s 2022 climate stress test incorporated physical climate risk scenarios and demonstrated that these risks can materially affect banks’ risk profiles. Similarly, the European Securities and Markets Authority (ESMA) has documented substantial exposure of EU investment funds to physical climate hazards.

In parallel with regulatory developments, an extensive academic literature has emerged to demonstrate how climate-related risks are reflected in asset prices and establish forward-looking methodologies such as short-term stress tests and long-term scenario analyses (which typically rely on integrated assessment models to quantify climate-related value-at-risk or evaluate changes in discounted cash flows under alternative temperature or policy pathways). However, these analyses are generally conducted at high levels of geographic and macroeconomic aggregation. While these are well suited for wide systemic risk assessments, investors lack further information granularity for strategic investment managements.

As such, this article presents a methodology that is directly applicable to institutional investors and asset managers who are looking to understand CPL for their own equity portfolios. This approach has the advantage of providing answers through a transparent and intuitive framework, without imposing onerous or resource-intensive data requirements.

Building and calibrating a Climate Physical Loss framework

The proposed Climate Physical Loss (CPL) framework rests on the principle that physical climate risk affects firm value through its impact on macroeconomic activity and, ultimately, on expected future cash flows. As such, a firm-level CPL is the difference between a firm’s baseline enterprise value and an alternative valuation in which future cash flows are scaled by macroeconomic losses attributable to physical climate risks.

Formally, the procedure consists of three steps: (i) quantifying country-level projected GDP losses as a function of temperature anomalies; (ii) transmitting these losses to firm valuations through a discounted‑cash‑flow framework; and (iii) reweighting relative valuation losses using sector‑level sensitivity scores.

Step 1: estimating regional GDP losses as a function of temperature anomalies

Country-level macroeconomic projections are sourced to obtain both the baseline trajectory of aggregate economic activity and the relative deviations from this trajectory induced by global temperature anomalies. Country-level deviations are sourced from NGFS scenario outputs[3].

The global non-linear effect of temperature on economic production has been empirically confirmed by Burke et al. (2015) and Newell et al. (2021), providing evidence for an inverted U-shaped relationship whereby average temperatures exceeding a turning point generate amplifying reductions in per capita GDP. To begin, we first estimate an aggregate damage function at the country-level, linking physical risk-induced country-level GDP damages (arising from both chronic and acute climate risk) to a non-linear function of global temperature anomalies, as emulated by NGFS MAGICC across scenarios and IAMs,

where global temperature anomaly  is measured relative to a reference year

is measured relative to a reference year  and where

and where  denotes the percentage deviation of real GDP from a no-damage baseline.

denotes the percentage deviation of real GDP from a no-damage baseline.

From the estimated aggregate damage function, nominal GDP growth factors under the baseline and physical-risk scenarios are defined as

where  denotes the aggregate price level. These factors scale firm-level cash flows in the valuation stage.

denotes the aggregate price level. These factors scale firm-level cash flows in the valuation stage.

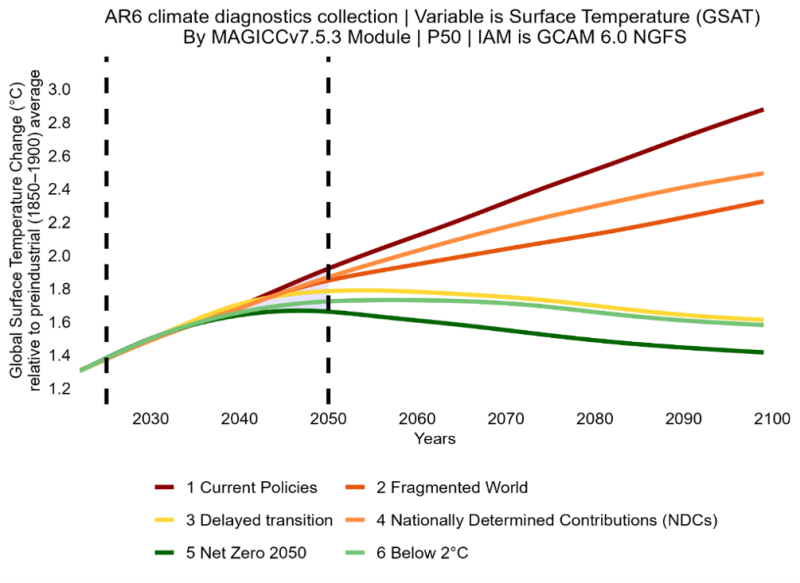

Figure 1: Global mean temperature scenario trajectories

Global temperature scenarios

Data from NGFS, IPCC. Interpolation under GCAM 6.0 NGFS IAM. Global surface temperature (GSAT) projection from the MAGICCv7.5.3 climate model, based on AR6 climate diagnostics used by NGFS Phase-V.

Step 2: Transmitting these losses to company valuations through a DCF model

The next stage is to incorporate those deviations into a discounted cash-flow (DCF) model: firm-level cash flows are assumed to grow with country nominal GDP and are discounted using sector-specific weighted average costs of capital (WACC).

The discount rates used in the discounted cash flow model are obtained from Damodaran’s publicly available estimates, which provide sector-level values for different regions[4].

From a model construction perspective, we can let firms be indexed by  , and denote by

, and denote by  the country of firm and by

the country of firm and by  its sector. Cash flows in the reference year are given by

its sector. Cash flows in the reference year are given by  . For horizon

. For horizon  to

to  , the baseline enterprise value follows[5]

, the baseline enterprise value follows[5]

where  is the sector- and region-specific discount rate (weighted average cost of capital). Under the physical-risk scenario:

is the sector- and region-specific discount rate (weighted average cost of capital). Under the physical-risk scenario:

Since is common to both valuations, the relative enterprise value loss simplifies to our primary impact metric,

Thus,  measures the proportional decline in firm value solely attributable to physical climate damages.

measures the proportional decline in firm value solely attributable to physical climate damages.

Step 3: Reweighting relative valuation losses using sector‑level sensitivity scores

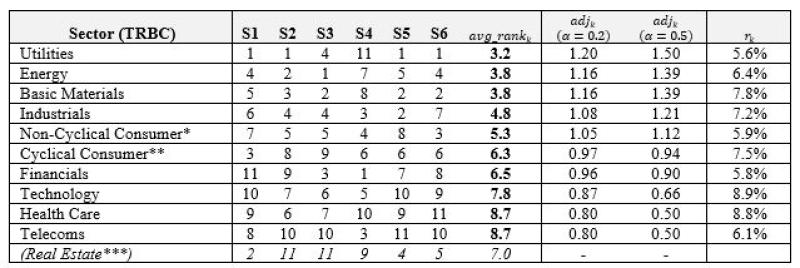

In the third stage, a final adjustment is applied to reflect the prevailing market assessment of the sensitivity of different sectors to physical climate risk. Various ESG data providers report scores measuring sectors’ perceived vulnerability to physical climate risk. Our model incorporates empirical evidence from Hain, Kölbel, and Leippold (2022), who compare six firm-level physical risk scores from commercial and academic sources. Although the providers differ markedly in methodology, the authors document substantial systematic variation across sectors: Utilities, Energy, and Materials consistently appear as the most exposed sectors, while Health Care, Communication Services, and Information Technology exhibit comparatively low exposure. This data is used to produce a sector-adjusted relative enterprise value loss such that losses are scaled upward in highly exposed sectors and downward in less exposed sectors[6].

Figure 2: Sector-specific characteristics

The seven first columns of this table from Hain, Kölbel, and Leippold (2022). They show sector rankings of six different ESG data providers based on the sensitivity of sectors to climate physical risks: Trucost (S1), Carbon4 Finance (S2), Southpole (S3), Truvalue Labs (S4), Sautner et al. (S5), and Kölbel et al. (S6).

Results: how exposed is the European market to physical climate risks?

Using the above model, we conducted empirical analysis focused on the 423 largest publicly listed European firms. This allowed us to assess:

- the climate physical risk sensitivity of different European countries;

- how sector-specific discount rates and sector-level exposure to physical hazards affect outcomes; and

- implications for European equity portfolio valuation.

Among the 15 countries considered, projected long-term economic outcomes exhibit substantial heterogeneity. Three clusters emerge in broad agreement with the literature on this topic (Burke et al., 2015; Kalkuhl and Wenz, 2020; Linsenmeier, 2023; Kotz et al., 2024; Schneider, 2025; Bilal and Känzig, 2026). Northern European countries face the mildest impacts, with projected economic trajectories ranging from a gain of approximately 5% for Finland to a loss of 16% for the Netherlands. A second group, including Belgium, Germany, Switzerland, and Austria, exhibits relatively homogeneous losses between 18% and 19%. By contrast, the southern economies incur substantially larger declines, with France, Italy, Spain, and Portugal all exceeding a 20% relative GDP loss by 2100.

A second determinant of climate-related economic damage is the underlying GDP growth trajectory. Holding other factors constant, economies with faster baseline growth experience larger current physical loss estimates, as higher future output amplifies the discounted impact of climate-induced deviations. Italy and Spain, which already feature among the most adversely affected countries in terms of 2100 GDP losses, also record the strongest baseline growth rates. This combination results in an increased present value of their projected CPLs. This is discussed further in Bouchet & Schneider (2026a).

Figure 3: Projected nominal GDP loss in Europe by 2100 under current policies

The figure reports, for each country of our sample, the projected relative loss in nominal GDP in 2100 under the NGFS Current Policies scenario (GCAM model), expressed as a percentage deviation from the corresponding baseline trajectory

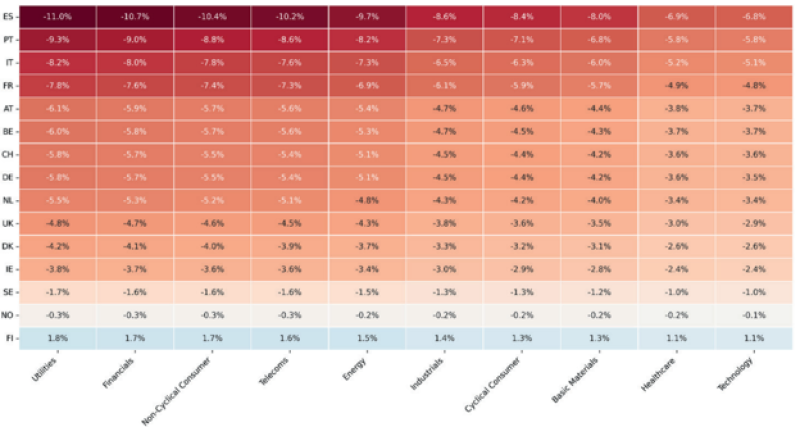

Next, we look at sector-level heterogeneity. Sectors such as Utilities or Non-Cyclical Consumer—which typically exhibit relatively low WACC—are valued on the basis of long-term cash-flows and are therefore more exposed when the distant flows are impacted by physical risks. Conversely, high-WACC sectors such as Technology are priced primarily on near-term cash flows, which makes their valuations less sensitive to physical risk shocks affecting distant flows. Incorporating this sectoral adjustment generates substantial dispersion in climate-induced valuation effects, with a ratio of approximately 1.6 between the most and least sensitive sectors (Figure 4).

Figure 4: Effect of sector-specific discount rate only on climate physical loss (CPL)

This heatmap displays the CPL for each country–sector pair after incorporating sector-specific discount rates. Sectors with low WACC tend to exhibit higher CPL as they are more sensitive to the long-term impact of climate change on their cash flows. Results are based on the NGFS “Current Policies” scenario, using the GCAM model at the 2100 horizon.

A second sectoral adjustment concerns the sectors’ perceived vulnerability to physical climate risks: certain sectors are more vulnerable to physical risks (e.g., Utilities, Energy, and Materials)[7]. Because the initial degree of vulnerability is specified in terms of a ranking, its conversion into a valuation relies on an additional parameter α that can take different values to modulate the influence on the final CPL. As  is difficult to estimate empirically, the analysis evaluates the sensitivity of results to alternative values, focusing on

is difficult to estimate empirically, the analysis evaluates the sensitivity of results to alternative values, focusing on  and

and  as plausible bounds. Results show that varying α not only alters the magnitude of CPL within a given country but may also change the ordering of the most affected sectors. This arises from the interaction with the discount-rate effect. For some sectors, such as Utilities, a relatively low discount rate is compounded by high vulnerability (i.e., a high adjustment factor) identified in the literature, whereas for other sectors, such as Financials, the effect of a low discount rate is dampened by their relatively low perceived vulnerability to physical risks[8].

as plausible bounds. Results show that varying α not only alters the magnitude of CPL within a given country but may also change the ordering of the most affected sectors. This arises from the interaction with the discount-rate effect. For some sectors, such as Utilities, a relatively low discount rate is compounded by high vulnerability (i.e., a high adjustment factor) identified in the literature, whereas for other sectors, such as Financials, the effect of a low discount rate is dampened by their relatively low perceived vulnerability to physical risks[8].

Application to a diversified Developed Europe equity benchmark

Within the sample of European countries and sectors, the estimated CPL spans a wide range, from –16.5% to +2.6% after adjustment to take into account the sectors’ perceived vulnerability to physical climate risks. Portfolio-level exposure is therefore highly sensitive to the underlying region and sector allocation. For the diversified Developed Europe equity benchmark, the portfolio-weighted CPL amounts to –4.7%. Figure 5 illustrates how alternative country and sector weightings would influence this result. Under an equal-weight allocation across all countries (15) and sectors (10) of our sample, the CPL would be –4.46%. Replacing equal sector weights with the benchmark’s sector weights slightly improves the CPL to –4.18%, implying a favorable sector-allocation effect. In contrast, applying the benchmark’s country weights while maintaining equal sector weights yields a CPL of –4.93%, corresponding to an adverse country-allocation effect. This decomposition suggests that the benchmark’s sector allocation slightly mitigates physical risk exposure, but that this relative gain from the sector effect is more than offset by a negative country-allocation effect. This can be traced back to the overweight positions in countries with higher physical risk exposure.

Figure 5: Climate physical loss of a diversified Developed Europe equity benchmark

The table reports the weighted physical climate loss (PCL) under alternative allocations. “Equal” allocates identical weights to each of the 15 countries (or 10 sectors) in the sample, while “Portfolio” applies the weights of the Developed Europe equity benchmark to the corresponding countries or sectors.

This framework offers a basis for producing estimates of ‘Climate Physical Loss (CPL)’ using a parsimonious, transparent and NGFS-aligned approach, but is not without caveat. We empirically show that estimated sensitivity parameters that structure the aggregate damage function in Step 1 are robust to the choice of NGFS scenario or integrated assessment model (IAM) and thus, scenario- and IAM-invariant[9]. This reflects the fact that IAMs operating under a given scenario must satisfy broadly similar aggregate carbon-budget constraints over the period. By contrast, while scenario selection is only modestly influential over outcomes over short time horizons (see the relatively narrow inter-scenario range depicted by the blue-shaded area circa-2050 in Figure 1), it becomes highly influential over long time horizons (as one would perhaps expect from Figure 1) since scenario-trajectories substantially diverge.

Conclusion: from climate risk assessment to strategic investment decision-making

Investors are increasingly required to provide robust assessments of the potential impact of physical climate risks on their equity portfolios. We contend that (1) it is feasible to perform these assessments in a parsimonious and regulator-compliant manner, without the need for asset-level or physical hazard data that creates an excessive burden on resources; (2) that these assessments can be done in an operationalized manner, making them directly transferable to strategic investment decision-making. We believe that the framework presented here achieves both (1) and (2) simultaneously. Moreover, the findings generated from this framework strongly showcase the importance of portfolio construction (i.e., accounting for the heterogeneous exposure of sectors and countries) in adjusting resilience to global temperature trajectories.

References

- Bilal, A., & Känzig, D. R. (2026). The Macroeconomic Impact of Climate Change: Global Versus Local Temperature. The Quarterly Journal of Economics, qjag011.

- Bouchet, V., & Schneider, N. (2026a). Physical Climate Risk in the European Equity Market: Quantifying Country – Sector Heterogeneity. Scientific Portfolio-an EDHEC Venture White Paper.

- Bouchet, V., & Schneider, N. (2026b). Physical Climate Risk in the United States Equity Market: Quantifying State – Sector Heterogeneity. Scientific Portfolio-an EDHEC Venture White Paper.

- Burke, M., Hsiang, S. M., & Miguel, E. (2015). Global non‑linear effect of temperature on economic production. Nature, 527(7577), 235–239.

- Kalkuhl, M., & Wenz, L. (2020). The impact of climate conditions on economic production: Evidence from a global panel of regions. Journal of Environmental Economics and Management, 103, 102360.

- Kotz, M., Levermann, A., & Wenz, L. (2024). RETRACTED ARTICLE: The economic commitment of climate change. Nature, 628(8008), 551-557.

- Linsenmeier, M. (2023). Temperature variability and long-run economic development. Journal of Environmental Economics and Management, 121, 102840.

- Schneider, N. (2025). The Global Geography of Long-Term Projected Macroeconomic Damages from Chronic Physical Risk and the Aggregation Problem. SSRN Working Paper.

Footnotes

[1] Physical Climate Risk in the European Equity Market: Quantifying Country-Sector Heterogeneity, Bouchet, V., Schneider, N. (2026a)

[2] NGFS Scenarios Portal, Network for Greening the Financial System

[3] The European economic sensitivity to a non-linear function of global temperature anomalies,  and

and  is estimated using the NGFS Phase 5 scenario dataset. This provides combinations of qualitative transition narratives and quantitative outputs from integrated assessment models (IAMs) that generate transition and physical-risk dynamics (e.g., REMIND, MESSAGE). For each scenario–model configuration, the NGFS reports projected country-level paths of real GDP. Rather than using these GDP projections directly, the dataset is used to re-quantify the relationship between global temperature anomalies and deviations of country-level GDP from baseline. Long-horizon nominal GDP projections are derived from two components: (i) a baseline scenario that represents the path of economic activity in the absence of climate damages through 2100, and (ii) a physical-risk scenario in which global temperature anomalies are mapped into country-level economic losses. For long-term projections (post-2050), the baseline real-activity path combines projections from the NGFS and the IPCC–SSP2 framework. Country-level deviations are generated by applying the estimated damage coefficients to an exogenous global mean temperature (GMT) trajectory. The sequence of global temperature anomalies is inserted into the quadratic damage function above to obtain non-linear and country-specific GDP deviations

is estimated using the NGFS Phase 5 scenario dataset. This provides combinations of qualitative transition narratives and quantitative outputs from integrated assessment models (IAMs) that generate transition and physical-risk dynamics (e.g., REMIND, MESSAGE). For each scenario–model configuration, the NGFS reports projected country-level paths of real GDP. Rather than using these GDP projections directly, the dataset is used to re-quantify the relationship between global temperature anomalies and deviations of country-level GDP from baseline. Long-horizon nominal GDP projections are derived from two components: (i) a baseline scenario that represents the path of economic activity in the absence of climate damages through 2100, and (ii) a physical-risk scenario in which global temperature anomalies are mapped into country-level economic losses. For long-term projections (post-2050), the baseline real-activity path combines projections from the NGFS and the IPCC–SSP2 framework. Country-level deviations are generated by applying the estimated damage coefficients to an exogenous global mean temperature (GMT) trajectory. The sequence of global temperature anomalies is inserted into the quadratic damage function above to obtain non-linear and country-specific GDP deviations  . When combined with the baseline GDP trajectory, these deviations yield the physical-risk and baseline GDP growth factors,

. When combined with the baseline GDP trajectory, these deviations yield the physical-risk and baseline GDP growth factors,  and

and  , which in turn determine the evolution of firms’ expected cash flows. For more information, see Physical Climate Risk in the European Equity Market: Quantifying Country-Sector Heterogeneity (Bouchet & Schneider, 2026a)

, which in turn determine the evolution of firms’ expected cash flows. For more information, see Physical Climate Risk in the European Equity Market: Quantifying Country-Sector Heterogeneity (Bouchet & Schneider, 2026a)

[4] Firm-specific discount rates are computed by assigning each TRBC sector to the appropriate set of Damodaran industry classifications. Information on the sector and country classification of stocks is sourced from CIQ, while the portfolio weights of stocks are taken from the Scientific Portfolio Capital Weight Regional Benchmark for Developed Europe.

[5]  is assumed to be far enough in the future to make any terminal value relatively negligible after discounting.

is assumed to be far enough in the future to make any terminal value relatively negligible after discounting.

[6] Again, for more details on the integration of these sensitivity scores into the enterprise value loss calculation, see Physical Climate Risk in the European Equity Market: Quantifying Country-Sector Heterogeneity (Bouchet & Schneider, 2026a).

[7] Data are taken from Hain, Kölbel, and Leippold (2022).

[8] For tables showing the results for this analysis, see Physical Climate Risk in the European Equity Market: Quantifying Country-Sector Heterogeneity (Bouchet & Schneider, 2026a).

[9] Parameters were estimated separately for each of the three IAMs that underpin the NiGEM outputs (GCAM 6.0 NGFS, MESSAGEix-GLOBIOM 2.0-M-R12-NGFS, and REMIND-MAgPIE 3.3-4.8) under each of the six NGFS Phase-V scenarios (Current Policies, Fragmented World, Delayed Transition, Nationally Determined Contributions, Net Zero 2050, and Below 2°C). Analysis also considered the degree of consistency between the scenario-based ranking of country-level vulnerability to physical climate risk and two widely used external benchmarks: the ND-GAIN Country Index and the Germanwatch Climate Risk Index. The objective was to evaluate whether countries identified as more climate-vulnerable in one system tend to occupy a similar position in the others. Overall, this demonstrated that the proposed ranking preserves the ordinal structure embedded in established climate-risk assessments. For more information, see Bouchet & Schneider (2026a).