- In this article, we use a new quantitative framework to demonstrate that climate change is an immediate macro-financial force that could reshape global markets.

- Macroeconomic Shifts: Rising temperatures slow structural economic growth through productivity declines and physical damages, while transition costs are likely to impose economic headwinds.

- Structural Risks: Real risk-free rates are expected to decline as investors price in the economic drag from damages. Meanwhile, increased climate-driven uncertainty fuels market volatility and tail risks, especially for long-duration assets.

- Market Revaluation: Under a 3◦C warming scenario, the equity risk premium is projected to rise by 15–25%, permanently driving down valuation multiples for risky assets. Adding dented cash flows from economic damages to the picture should concern both long-term investors and policy makers.

Climate change is no longer a distant environmental concern. It is an immediate macro-financial force that is reshaping global economic growth, financial stability, asset returns, and investor behaviour for the coming decades. Yet the financial impacts of climate change are often misunderstood or incompletely captured by traditional, backward-looking risk models. This article distils the insights of an advanced climate–finance model into implications for policymakers and investors.

Our central finding is clear: with rising temperatures, economic growth slows lastingly, financial uncertainty increases, and investors demand significantly higher compensation for risk. As a result, even in the absence of catastrophic tipping points, under a 3◦C warming scenario, the equity risk premium (ERP) rises by c. 15–25%, while the real risk-free rate temporarily declines and valuation multiples permanently recede for risky assets. These effects are large enough to meaningfully affect valuations across equity and fixed-income markets. The results highlight how climate channels affect financial stability and why forward-looking modelling tools are essential.

Four forces emerge linking climate to financial markets:

- Physical damages. Rising temperatures slow long-run economic growth. Productivity declines, labour capacity shrinks in heat-exposed regions, and global output falls relative to historical expectations. Simultaneously, the frequency and intensity of extreme climatic events rise, disrupting economic activity in potentially lasting ways.

- Transition costs. Potentially transitioning to a low-carbon economy requires resources. Investment, regulation, and carbon pricing impose costs as they reduce long-run damages.

- Volatility effects. Temperature increases raise uncertainty, making markets more sensitive to climate-related shocks. Economic volatility, policy uncertainty, and climate-linked shocks raise required returns on risky assets.

- Tempering loop. Economic growth uncertainty propagates into temperature uncertainty. That is to say: higher-than-expected economic activity translates into higher-than-expected temperatures, which results in higher-than-expected damages to consumption growth, and vice versa.

The model combines these channels into a single framework that provides quantitative, forward-looking estimates under plausible warming scenarios. The combination of these forces leads to:

1. Unprecedented climate reality calls for a new asset pricing toolkit

Financial markets are forward-looking. Investors base pricing and portfolio decisions not only on current economic conditions but on expectations about future consumption, productivity, and uncertainty. Climate change fundamentally alters these expectations.

Financial markets have begun to incorporate climate risk, but often in a fragmented or backward-looking manner. Traditional risk models assume stationary economic dynamics and stable long-run growth patterns. Climate change breaks these assumptions. Rising temperatures, shifting precipitation patterns, and the increased frequency of extreme weather introduce structural changes that affect productivity, capital accumulation, and consumption growth.

In contrast, modern empirical research demonstrates that temperature increases reduce global productivity, climate volatility rises with warming, while economic damages persist for long periods.

At the same time, climate policy—whether through carbon pricing, regulation, clean-energy investment, or global agreements—generates its own macro-financial effects. These transition forces can either amplify or mitigate physical damages.

Historical financial data cannot fully capture these unprecedented dynamics. Backwards-looking approaches struggle to incorporate these structural changes, because the world is entering a future with no historical precedent. For this reason, climate-change economics must rely on structural, physics-aware, calibrated models. The academic framework underlying this article connects:

- a physical climate module (capturing temperature trends, uncertainty, and policy targets);

- a long-run risk (Bansal and Yaron, 2004) macroeconomic model widely used in asset pricing;

- empirically calibrated channels for damages, transition costs, and volatility.

By embedding climate directly into the drivers of consumption growth, the model generates closed-form formulas for core financial quantities such as the risk-free rate, the ERP, and price-dividend ratios. This article explains what these results mean for financial markets in a warming world.

2. Why global temperatures matter for asset pricing

Financial asset values depend on expectations about future cash flows and on how these cash flows are discounted. If climate change lowers expected economic and consumption growth, or increases their uncertainty, investors require more compensation for bearing additional risks. In equilibrium, this is reflected in asset prices, the risk-free rate, and the ERP. Temperature affects macroeconomic conditions through three fundamental channels.

1. Physical damages

Empirical evidence shows that persistent increases in temperature reduce productivity (especially outdoor labour), agricultural yields, manufacturing efficiency, health outcomes, and ultimately GDP. Moreover, as temperature rises, extreme climate events (e.g., wildfires, droughts, floods) also increase in frequency and acuteness. These effects accumulate over time. Even small yearly reductions compound into substantial long-run output losses.

Quantitative studies estimate global GDP losses of 20-30% in moderate warming scenarios, and over 40% in high-warming cases (see e.g., Burke, Hsiang and Miguel (2015); Kotz, Levermann and Wenz (2024); Bilal and Känzig (2024)). These impacts evolve gradually but persist over roughly a decade for each additional temperature increment.

2. Transition Costs

Mitigation policies (e.g., carbon pricing, clean-energy investments, regulation) can slow or reverse warming but require economic resources and create economic headwinds. The model captures this through a policy state that gradually adjusts temperature trajectories but impacts near-term consumption.

3 Temperature-Driven Uncertainty

A growing body of academic studies (see e.g., Addoum, Ng and Ortiz-Bobea (2020) or Barnett, Brock and Hansen (2020)) finds that hotter years also tend to be more volatile. Variability increases in rainfall and crop production. Energy demand becomes more uncertain. Supply chains experience more climate disruption. Altogether, weather-sensitive production fluctuates more with warming.

In financial models, higher uncertainty raises risk premia, which particularly impacts long-duration assets.

Within a reduced-form model, one captures these three channels in a streamlined way: temperature affects consumption, policy affects temperature, and both interact with economic uncertainty.

As a result, financial markets price climate outcomes long before they materialize.

3. How to price climate risks? A dual-module framework

3.1 Climate module captures both temperature and policy uncertainties

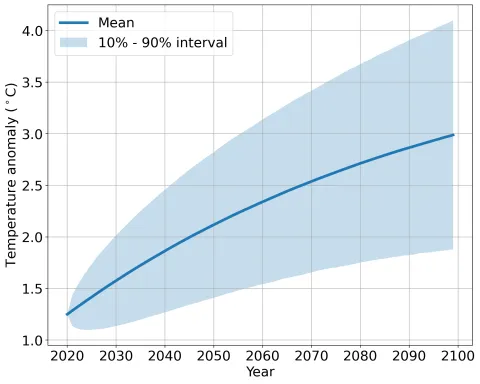

The climate block of the framework specifies coupled stochastic dynamics for the strength of climate policy and the resulting global mean temperature anomaly. It uses a simple double mean-reverting process: one state variable captures the policy state, and the other tracks temperature conditional on that policy. The parameters are chosen so that the median of the temperature remains close to the reference NGFS “Current Policies” projections, with an expected temperature anomaly of 3°C by 2100. The uncertainty parameters are calibrated to represent plausible dispersion around the expectation. This dispersion arises from uncertainty around the calibrated “Current Policies” specification.

Figure 1 provides a simple illustrative example: the median of the simulated temperature paths and the confidence intervals given by the uncertainties

Figure 1: Temperature potential trajectories

Notes: The 10% percentile path, 50% percentile path and 90% percentile path of the simulated temperatures.

3.2 Economic module incorporates climate-change impacts

The model incorporates two types of climate-related economic impacts:

1. Physical Damages

Recent empirical work (see e.g., Burke, Hsiang and Miguel, 2015; Kotz et al., 2024; Bilal and Känzig, 2024) indicates that a 3°C world could face long-run global GDP losses ranging from 20% to more than 40%. The model uses estimates around the mid-range of these values and translates them into a gradual but sizable drag on consumption growth. Damages are not assumed to be permanent but instead persistent, lasting roughly a decade for each incremental temperature rise. In practice, this means that a sequence of warmer-than-expected decades can generate long-lived slowdowns in activity, while cooler-than-expected periods only partially offset these losses. This persistent but non-permanent damage structure is designed to remain consistent with the empirical literature, while preserving enough flexibility to explore different outcomes.

2. Transition Costs

Transition costs capture the economic drag associated with moving away from fossil fuels. These include capital expenditures for low-carbon technologies, changes in energy mix, stranded assets, and regulatory or policy adjustments that affect production costs and relative prices. In the model, mirroring reality, transition costs arise whenever policy targets deviate from business-as-usual warming. They generate a hindrance on economic growth when policies become more stringent, and can be interpreted as a transient subsidy when targets are relaxed or delayed, as carbon-intensive activities face fewer constraints. Formally, transition costs enter the consumption growth process as an additional component, whose sign and magnitude are calibrated to reflect the projected transition costs by NGFS transition scenarios.

The result is a consumption growth process that slowly declines as temperatures rise and which adjusts depending on the acuteness of policy commitments.

4. What are the impacts on the financial market?

4.1 Sagging risk-free rate

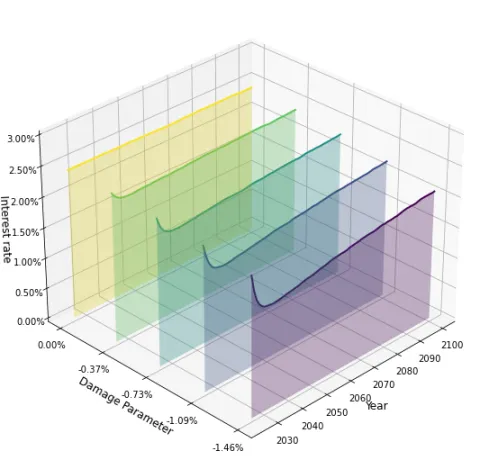

In our framework, a key result concerns the behaviour of the real risk-free rate in a warming world. As temperatures rise and climate damage accumulates, expected long-run consumption growth declines. Because the equilibrium real risk-free rate is tightly linked to the expected path of aggregate consumption, this slowdown translates into a decline in the real risk-free rate, particularly pronounced between 2030 and 2050. Intuitively, when future consumption is expected to grow more slowly, agents place a higher value on future consumption relative to today, which lowers the real risk-free rate consistent with intertemporal optimality.

This effect is, however, transitory rather than permanent. Once temperatures and climate policies jointly lead the system toward a more stable state, the economy partially adapts. Expected consumption growth stops deteriorating further, and the real risk-free rate gradually converges back toward its long-run level implied by preferences and trend productivity. In other words, the fall in real risk-free rate is a transitional response to a period of heightened climate-induced growth risk, not a permanent feature of the system.

Figure 2 illustrates this mechanism for different values of the damage parameters: stronger climate damages amplify both the depth and the duration of the temporary decline in the real risk-free rate. This behaviour has direct implications for sovereign debt sustainability, the choice of discount rates by pension funds and insurance companies, and the pricing of inflation-linked and other long-term fixed-income instruments. Real risk-free rates may fall during the decades in which climate risk increasingly weighs on expected growth, but this climate discounting effect weakens as the system transitions toward a new long-run equilibrium.

Figure 2: Risk-free rate time-profile for different damages

Notes: Time-profile of the risk-free rate rf,t on the mean trajectory of the state-variables

when the damage parameter decreases from counterfactual (0%) to high damage (−1.46%) calibration.

4.2 Magnified ERP

While the risk-free rate falls, the ERP rises substantially. In our simulations, this occurs because the consumption risks associated with warming—lower long-run growth, higher volatility, and temperature-related shocks—become more important to investors. Under a 3°C scenario, the ERP increases by roughly 15–25% relative to today’s levels, meaning that the investors require a noticeably higher compensation for bearing equity risk.

The ERP represents the extra return investors demand for holding risky assets. In our framework, it can be decomposed into several sources of risks: short-run economic uncertainty, long-run growth uncertainty, temperature-linked damage uncertainty, policy uncertainty, and volatility-related uncertainty.

In the climate-augmented framework, the ERP rises because:

- physical damages amplify downside risks to consumption growth;

- policy uncertainty around the transition path introduces additional macroeconomic shocks; and

- higher temperatures increase volatility, making future consumption and dividends more uncertain.

In the long-run risk framework, the long-run component of the ERP is proportional to the covariance between the stochastic discount factor and news about the long-run consumption growth. When we augment the model with climate damages and policy, part of the long-run growth uncertainty correlates with temperature uncertainty, which in turn mutes the original variability. This natural moderation mechanism slightly reduces the long-run risk ERP contribution. However, this reduction is more than offset by the increase from physical damages, transition uncertainty, and volatility effects.

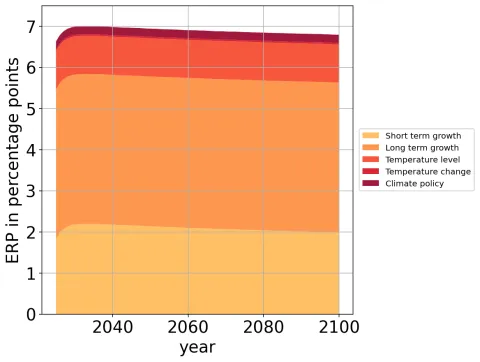

Figure 3 offers an intuitive decomposition of these contributions. Different colour blocks from the bottom to the top represent the ERP coming from the short-run consumption risk, the long-run consumption risk, the temperature level risk, the temperature change risk and the policy risk.

Figure 3: ERP composition time-profile

Notes: Time-profile of the ERP on the mean trajectory of the state-variables at reference calibration.

In our calibration, the ERP in a 3°C warming scenario is projected to be 1525% higher than the counterfactual case. This upward shift in the ERP mechanically implies lower valuation multiples (price-dividend and price-earning ratios), with the largest impact on assets with long-duration cash flows, such as technology and growth equities, infrastructure and utility assets, and issuers in emerging markets that are highly exposed to physical climate risk.

5. Structural implications for investors and policymakers

Investors face a new macro-financial regime defined by climate-adjusted expectations. Both equity and bond markets should be impacted. Higher ERP means equities must compensate investors through higher expected returns, lowering valuations in the near term. Bond markets may see depressed real yields during the warming period. Furthermore, temperature-driven uncertainty increases the probability of extreme negative outcomes in long-term cash flows, hence increasing tail risks. Portfolios with high exposure to long-horizon cash flows (technology, infrastructure, utilities) are especially exposed. Also, sectors sensitive to policy and energy costs (utilities, materials, heavy industry) face significant repricing risk on potentially volatile transition pathways. Conversely, one should record a rise of climate hedging solutions, from an almost non-existent current state.

Policymakers are also in for a rocky warming century. As climate pathways shape macro-financial stability, policymakers should anticipate higher market volatility as global warming extends into more acute territories, together with stronger linkages between climate policy and financial conditions. In this environment, macroprudential frameworks may need to incorporate long-horizon climate risks rather than focusing on catastrophe losses. Aware climate policies could prevent blunders. First, the financial system’s sensitivity to climate trajectories underscores the importance of stable, credible transition pathways. Second, stable regulatory environments and credible long-term temperature commitments can reduce uncertainty and dampen the rise in risk premia.

To sum up, climate change fundamentally reshapes the structure of asset returns. Even without accounting for catastrophic tipping points, global warming introduces long-run consumption risks that significantly alter the pricing of bonds and equities. A warming trajectory toward 3◦C is sufficient to generate measurable increases in the ERP and declines in the risk-free rate. For investors, this means the cost of capital rises; for policymakers, it signals that financial stability will depend increasingly on the climate pathway the world follows.

This article provides an accessible translation of a rigorous climate-finance model. While simplified, the framework illustrates a central idea: climate change is not just an environmental challenge, it is a macro-financial transformation whose consequences will unfold steadily over decades.

References

Addoum, J. M., Ng, D. T., and Ortiz-Bobea, A. (2020). Temperature Shocks and Establishment Sales. The Review of Financial Studies, 33(3):1331–1366.

Bansal, R. and Yaron, A. (2004). Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles. The Journal of Finance, 59(4):1481–1509.

Barnett, M., Brock, W., and Hansen, L. P. (2020). Pricing Uncertainty Induced by Climate Change.

The Review of Financial Studies, 33(3):1024–1066.

Bilal, A. and Känzig, D. R. (2024). The Macroeconomic Impact of Climate Change: Global vs. Local Temperature. NBER working paper.

Burke, M., Hsiang, S. M., and Miguel, E. (2015). Global Non-Linear Effect of Temperature on Economic Production. Nature, 527(7577):235–239.

Kotz, M., Levermann, A., and Wenz, L. (2024). The economic commitment of climate change. Nature, 628(8008):551–557. Retracted 3 December 2025