- Climate change creates financially material risks for infrastructure assets through physical risks from climate hazards and the transition dynamics associated with the shift towards a low-carbon economy, with direct implications for long-term asset valuation.

- Scientific Climate Ratings develops forward-looking climate risk assessments based on scientific modelling, high-resolution geospatial data, extensive financial datasets and climate research from the EDHEC Climate Institute.

- Our Climate Risk Rating (CRR) quantifies the financial materiality of climate risks by translating physical and transition risks into percentage impacts on net asset value, using a valuation-based, scenario-driven framework.

- Applying CRR across a global infrastructure asset universe indicates that climate risk impacts vary across assets, depending on sector characteristics, location and asset risk exposure.

- For institutional investors, CRR supports the integration of climate risk into valuation, due diligence and portfolio risk management decisions.

Introduction: Climate Risk as a Financial Variable in Infrastructure Investment

Infrastructure assets are central to the low-carbon transition and simultaneously on the front line of climate change impacts. Their long lives, capital intensity, functional specificity, and location dependence make them particularly exposed to both the physical consequences of a changing climate and the economic effects of the transition to a low-carbon economy. Unlike corporate assets, they typically serve a fixed purpose and operate under long-term contractual or regulatory frameworks. This limits their ability to adapt activities in response to policy or market demands and increases stranding risks.

Infrastructure investments are predominantly held by institutional investors with inherently long-term horizons and liabilities. Their climate risk therefore moves beyond a peripheral sustainability concern and becomes a central determinant of long-term asset valuation and risk management.

Despite this, climate risk is still often assessed using backwards-looking indicators or exposure metrics that are difficult to reconcile with standard investment practice. Such approaches may signal vulnerability, but are rarely sufficient to answer the question that ultimately matters for investors: How will climate risk affect asset values in the mid- to long term? Without accounting for developments in climate change and their related economic impacts, it remains difficult to integrate climate risk into asset pricing, portfolio construction, and risk management decisions.

In this article, we address this gap by presenting a valuation- and climate scenario-based framework for measuring the financial materiality of climate risk for infrastructure assets. Scientific Climate Ratings and the EDHEC Climate Institute used this framework to develop the CRR – using a rating scheme that compares assets based on their current and future climate risks. Building on established discounted cash-flow methodologies, we integrate physical and transition risk data into financial valuation models to estimate the impact on assets’ NAV across a range of forward-looking climate scenarios until 2035 and 2050. This allows climate risks to be expressed in the same language investors already use to assess performance and risk.

Focusing on a global universe of infrastructure assets across all TICCS[1] sectors and major economies, we show that climate risk is highly heterogeneous, asset-specific, and dynamic. While some assets experience limited valuation effects over the medium term, others exhibit material changes in expected value once physical and/or transition risks are embedded in the valuation models. Importantly, we also demonstrate that resilience and decarbonisation strategies can significantly alter these outcomes when implemented effectively.

Why climate risk has become a valuation issue for infrastructure

Infrastructure investment has traditionally been associated with stable cash flows, inflation protection, and resilience across economic cycles. These features have made this asset class particularly attractive to institutional investors seeking long-duration, predictable returns. Climate change, however, challenges several of the assumptions underlying this perception.

First, infrastructure assets are fundamentally shaped by their location, which determines their exposure to physical climate risks. Climate change not only increases the frequency and severity of hazards such as floods, storms, wildfires, and heat stress, but also exposes regions and locations that were not historically considered at risk. Many infrastructure assets were designed and built under past climate conditions and are therefore not fully adapted to the evolving hazard landscape.

At the same time, infrastructure assets are long-lived and largely immobile. Transport hubs, energy generation facilities, utilities, and data infrastructure are fixed to specific geolocations for decades and cannot be relocated once built. As a result, increasing physical hazards can translate into persistent operational disruptions, repair costs, and revenue losses over time. Even when individual events are manageable, repeated disruptions can materially alter long-term cash-flow profiles and asset valuation (Mandel et al., 2025).

Second, infrastructure assets are deeply embedded in the transition to a low-carbon economy. Policies designed to reduce greenhouse-gas emissions — such as carbon taxes — directly affect cash flows, particularly for high-emitting assets. At the same time, shifts in demand, regulation, and technology can alter revenue trajectories across sectors. These transition dynamics are not abstract policy risks; they are financial drivers that influence both revenues and costs.

Third, the extended time horizons of infrastructure investments amplify the importance of forward-looking analysis. Climate risks that may appear modest over the next few years can become economically material over horizons that are highly relevant for pension funds and other long-term investors. Ignoring these effects risks systematically mispricing assets and underestimating downside risk. For these reasons, forward-looking climate risk must be incorporated directly into the valuation frameworks that underpin investment decisions.

What financial materiality means in practice

In an investment context, financial materiality refers to the extent to which a risk affects an asset’s economic value. For infrastructure, this ultimately means understanding how climate-related factors alter future cash flows and, through discounting, NAV.

A valuation-based approach to climate risk starts from a simple premise: The value of an infrastructure asset today reflects the present value of the sum of all cash flows it is expected to generate in the future. Climate risks become financially material when they change either the level or the timing of those cash flows. For example, physical risks can increase capital expenditures through damage and repairs, raise operating costs, or reduce revenues through business interruption. Simultaneously, transition risks can increase costs through carbon taxes or alter revenues as market preferences evolve.

Expressing climate risk as a relative impact on NAV provides an intuitive, decision-relevant metric. Unlike abstract scores, valuation impacts can be directly compared across assets, incorporated into pricing models, and aggregated at the portfolio level. They also allow investors to distinguish between assets that face similar exposures but very different financial consequences.

Importantly, materiality is not uniform across infrastructure. Assets differ in their exposure to hazards, emissions profiles, regulatory environments, and adaptability. As a result, climate risk affects infrastructure assets in different ways. By quantifying impacts on NAV at the asset level, the CRR highlights how physical and transition risks can lead to materially different valuation outcomes for individual assets, including under more adverse climate conditions.

Methodology: From Climate Science to Cash Flows – Integrating Climate Risk into Infrastructure Valuation

Assessing the financial materiality of climate risk requires a valuation framework consistent with how infrastructure assets are priced in practice and forward-looking valuation techniques that reflect expected future cash flows, accounting for climate risks.

Valuing infrastructure assets using a discounted cash-flow approach

Because most infrastructure investments are privately held and lack observable market prices, we use a discounted cash flow approach (Jayles & Shen, 2024) to value infrastructure assets, consistent with the principles set out in IFRS 13 for fair value measurement and with standard market practice for unlisted infrastructure equity investments (IFRS, 2025). Under this approach, an asset’s value at any point in time is defined as the present value of the cash flows it is expected to generate in the future.

In the context of the CRR, valuation focuses on decision-relevant time horizons rather than full asset maturity. NAV is therefore computed using projected cash flows up to 2035 and 2050. While this represents a partial NAV rather than a full-life valuation, it reflects the horizons most relevant for investment decisions, risk management, and strategic asset allocation in institutional portfolios.

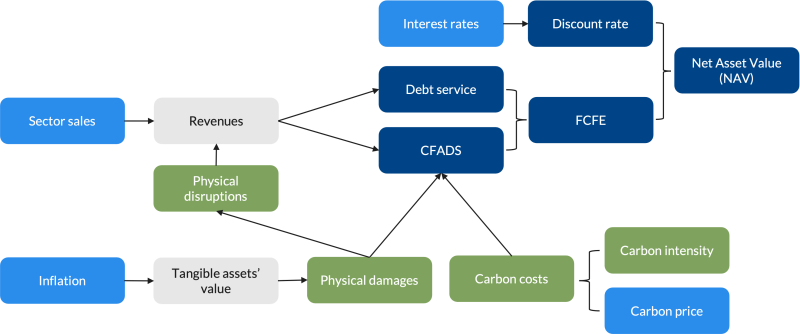

Future cash flows are discounted using a scenario-dependent discount rate that combines a country-specific risk-free rate (calculated from the climate scenario data) with an equity risk premium[2]. Risk-free rates are derived from the macroeconomic projections of short- and long-term interest rates embedded in each climate scenario (see Figure 1 for a full overview of the considered variables and their relations).

Figure 1: From climate hazard to asset valuation: The climate risk model that builds the base for the CRR

The macroeconomic variables at the country level are provided for each climate scenario (light blue), while the forward-looking climate risk variables are available at the asset level (green). For the financial variables, we differentiate between the baseline financial inputs (grey) and the calculated output variables of the asset pricing model (dark blue).

Revenue-driven cash flow projections

Revenues play a central role in determining infrastructure cash flows and, therefore, asset value. To integrate climate scenarios into revenue modelling, we apply a sector- and country-specific approach that links company revenues to sectoral sales projections derived from the climate scenarios.

Revenues are decomposed into price movement and production growth. Because many infrastructure assets operate near full capacity, production volumes are assumed to be capped or to decline for regulated or capacity-constrained assets. In contrast, price movements reflect differences between nominal and real-sector growth under each climate scenario. Sectoral sales projections are derived using mappings between NACE classifications (Eurostat, 2023) and TICCS, ensuring consistent and comparable treatment across infrastructure sectors.

The resulting revenue trajectories are projected annually up to 2050 and feed directly into the estimation of cash flows used in the discounted cash flow valuation.

Incorporating future physical and transition risks into cash flows

Climate risks affect infrastructure valuation by altering expected cash flows relative to a reference case without climate-related shocks. These effects enter the valuation model through both physical risks and transition risks.

Physical risks affect infrastructure assets through two mechanisms. First, climate hazards can cause direct damage to physical assets, increasing capital expenditures and operating costs. Second, they can disrupt operations, resulting in revenue losses due to downtime and reduced productivity. Hazard severity and frequency are projected over time using climate scenario information, allowing expected damages and disruptions to evolve consistently with future climate conditions.

Transition risks affect cash flows through two main channels. First, carbon costs, specifically carbon tax, increase operating costs, especially for assets with high direct emissions. Second, changes in market preferences and regulation can alter demand and pricing dynamics across sectors. These effects unfold over time and depend on both policy trajectories and sector-specific characteristics.

Finally, macroeconomic effects reflect the broader economic consequences of climate change and climate policy. Changes in GDP, inflation, and interest rates influence revenues and discounting assumptions in valuation models. While these effects are systematic rather than asset-specific, they form an important part of the overall climate risk environment in which infrastructure assets operate.

By explicitly modelling these channels, climate risks can be integrated into standard discounted cash-flow analysis without departing from established valuation practice.

Defining climate risk through relative valuation impacts

To quantify climate risk in financial terms, we define risk as the relative difference in NAV between a climate-risk condition and a reference condition. In the reference condition, exposure to physical hazards and carbon costs is deactivated, and revenues grow in line with inflation. Climate-risk conditions activate impacts from physical risks, transition costs, or both.

Climate risk is inherently forward-looking and uncertain. Single-path projections are ill-suited to capture the range of plausible futures facing long-lived infrastructure assets. To address this, we assess valuation impacts across a range of climate scenarios, including orderly transition, disorderly transition, and no transition scenarios, which are characterised by continued policy inaction. Rather than focusing on individual scenarios in isolation, we compute the expected valuation outcome by weighting scenario-specific results according to their probability of occurrence (Rebonato et al., 2025)[3]. This expected NAV serves as a reference point for comparing risks across scenarios and assets.

Based on the relative NAV differences, we derive quantitative metrics for physical, transition, and overall climate risk. These valuation-based metrics underpin the CRR, ensuring that the ratings reflect the direct financial impact of climate risk on infrastructure asset value. Simultaneously, the probabilistic approach avoids embedding overly optimistic assumptions about future policy or technology pathways into valuation results. For investors, this provides a realistic, internally consistent framework that integrates the full range of climate outcomes into valuation, supporting risk-aware decision-making under uncertainty.

Results: Using a Valuation-Based Framework to Assess Climate Risk in Infrastructure

Applying the valuation-based framework, we assess the financial impact of climate risk across a global universe of nearly 500 infrastructure assets spanning eight TICCS superclasses and 24 countries[4]. The framework integrates physical and transition risks into asset-level valuation analysis across two future horizons and multiple climate scenarios, producing CRR.

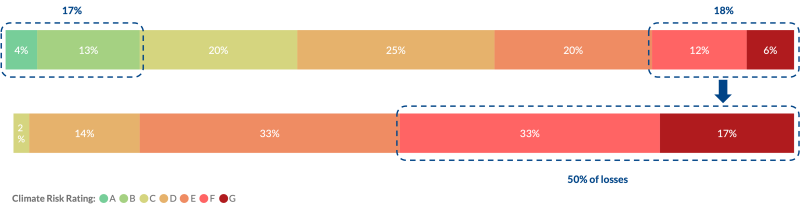

Figure 2 highlights a key empirical result: climate-related valuation losses are highly concentrated across assets. While the overall CRR distribution is close to symmetric, assets in the two lowest rating categories (F and G), representing around 18 percent of the asset universe, account for more than 60 percent of total expected NAV losses. By contrast, assets rated A and B are associated with positive valuation effects and are therefore excluded from the loss-concentration view.

Figure 2: Climate Risk Rating (top) and loss distribution (bottom) across rating classes based on the Expected Scenario by 2050

* Assets rated with A and B are excluded from the graph because they are associated with positive impacts on NAV, seeing an average increase in NAV of 9 percent for A-rated assets and 2.5 percent for B-rated assets.

This concentration of losses underscores the uneven distribution of climate-related financial risk within infrastructure portfolios. From an investment perspective, it implies that a relatively small subset of assets can drive a disproportionate share of downside risk, reinforcing the value of tools that allow investors to identify, benchmark, and prioritise climate risk at the asset level.

The results further demonstrate that climate-related valuation impacts vary across infrastructure assets depending on asset and sector characteristics, geographic location, and exposure to physical hazards and transition dynamics. Some assets exhibit limited valuation sensitivity to climate risk over the medium term, whereas others face material expected NAV losses, particularly at longer horizons. Physical risks tend to dominate for assets located in regions and areas more exposed to hazards such as floods or storms, while transition risks are more prominent for high-emitting assets or those operating in sectors undergoing rapid structural change.

By quantifying climate risk directly in valuation terms and providing a transparent breakdown of contributing factors, the CRR framework enables consistent comparison of climate-related financial impacts across assets, sectors, and geographies.

How climate risk evolves over time: resilience, decarbonisation, and value

The CRR framework is forward-looking by design and reflects the evolving nature of climate risks over time. While baseline assessments capture the systematic impact of physical and transition risks, asset-specific information can materially alter valuation outcomes. To this end, the framework can include both current and future company-specific decarbonisation and resilience strategies.

These adjustments rely on the ClimaTech database developed by the EDHEC Climate Institute, which provides evidence-based assessments of decarbonisation and resilience strategies and their effectiveness across infrastructure sectors (EDHEC Climate Institute, 2025). Decarbonisation strategies – such as reducing direct emissions or shifting to lower-carbon technologies – can mitigate transition risks by reducing exposure to carbon pricing and regulatory change. Resilience strategies — such as flood defences or storm-resistant design – can reduce expected damage and business disruptions from physical hazards.

When supported by credible data, we adjust projected emissions, expected damages, operational disruptions, and associated costs. This allows the CRR to reflect both current exposures and the potential impact of implemented or planned climate strategies on future asset valuations, while maintaining transparency and consistency across the rated universe (see an example of the adjustment process in the Use Case box). This approach allows investors to distinguish between assets that are exposed to high climate risk and those that combine high exposure with credible mitigation and adaptation pathways.

Implications for Institutional Investors

For institutional investors, the CRR provides a practical and structured tool for integrating climate risk into infrastructure investment analysis. By expressing climate risk directly in valuation terms, the framework complements existing financial models and supports asset-level assessment and comparison.

Specifically, the CRR offers insights into how physical and transition risks affect future cash flows and asset values under different climate scenarios and time horizons. The ratings also enhance transparency by clearly identifying the drivers of climate risk, including physical hazards, transition dynamics, macroeconomic developments, and asset-specific characteristics.

As such, the CRR supports the integration of climate risk considerations into valuation, due diligence, and strategic decision-making processes for infrastructure investments.

Conclusion: Making Climate Risk Measurable and Actionable in Infrastructure Investment

Climate change increasingly shapes the financial outlook and risk landscape of infrastructure assets and investments. By translating physical and transition risks into valuation impacts, the forward-looking framework developed by the EDHEC Climate Institute and Scientific Climate Ratings makes climate risk measurable, comparable, and actionable for infrastructure investors.

The results presented in this paper illustrate how a valuation-based, scenario-driven approach can capture asset-specific climate risk impacts and reflect the role of effective resilience and decarbonisation strategies that can materially alter asset valuation. The CRR provides investors and asset owners with a practical tool for estimating the long-term viability of infrastructure investments and integrating climate risk considerations into their decision-making. It is therefore not an optional refinement, but a necessary step toward informed long-term capital allocation in a changing climate.

Footnotes

[1] The Infrastructure Company Classification Standard (TICCS) provides investors with a frame of reference for approaching the infrastructure asset class. It offers an alternative to investment categories inherited from the private equity and real estate universe, which are less informative when classifying infrastructure investments (SIPA, 2025b).

[2] As of January 2026, the equity risk premium is kept constant and independent of any climate scenario.

[3] ECI developed a methodology to calculate the probability of each climate scenario happening (Rebonato et al., 2025). Our climate risk model uses these probabilities to calculate the expected NAV, which serves as a reference for evaluating different types of risk. More de s on the climate scenario methodology can be found in our technical documentation.

[4] This universe is based on Scientific Infra & Private Assets’ Unlisted Infrastructure Universe, a database of tracked assets that represent the fair value- and risk-adjusted performance of the unlisted infrastructure asset class. In total, it includes 9,100 unique infrastructure companies in the 27 most active national markets for infrastructure investors to define an investible universe of private infrastructure companies. These companies have a minimum of USD 1 million in total asset book value, are privately owned, and can be categorised using TICCS (SIPA, 2025a).

References

- EDHEC Climate Institute (2025). The ClimaTech project: Assessing infrastructure decarbonisation and resilience strategies. EDHEC Climate Institute. Last accessed on October 2, 2025. https://climateinstitute.edhec.edu/climatech-project

- Eurostat (2023). Glossary: Statistical classification of economic activities in the European Community (NACE). Eurostat, Statistics Explained. Last accessed on October 2, 2025. https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Glossary:Statistical_classification_of_economic_activities_in_the_European_Community_(NACE)

- IFRS (2025). IFRS 13 fair value measurement. IFRS (International Financial Reporting Standards) Accounting Standards Navigator. Last accessed on October 2, 2025. https://www.ifrs.org/issued-standards/list-of-standards/ifrs-13-fair-value-measurement/

- Jayles, B. & Shen, J. (2024). Computing extreme climate value for infrastructure investments. Asset pricing applied to NGFS Phase 4 and Oxford Economics scenarios to measuring climate risks at the asset level. SSRN. https://dx.doi.org/10.2139/ssrn.4779788

- Mandel, A., Battiston, S., & Monasterolo, I. (2025). Mapping global financial risks under climate change. Nature Climate Change, 15(3), 329-334. https://doi.org/10.1038/s41558-025-02244-x

- Rebonato, R., Melin, L., & Zhang, F. (2025). Climate scenarios with probabilities via maximum entropy and indirect elicitation. SSRN. http://dx.doi.org/10.2139/ssrn.5128228

- SIPA (2025a). Global universe standard for infrastructure investment benchmarking. Scientific Infra & Private Assets. Last accessed on October 2, 2025. https://docs.sipametrics.com/docs/infrastructure-universe-standard

- SIPA (2025b). The Infrastructure Company Classification Standard (TICCS). Scientific Infra & Private Assets. Last accessed on October 2, 2025. https://docs.sipametrics.com/docs/ticcs

Technical Documentation

For full details on our Climate Risk Ratings, see: