- Historical and cross-sectional attribution analysis of greenhouse gas emissions associated with financial portfolios has received little attention. Understanding the drivers that influence these emissions is essential to help portfolio managers set reduction targets and avoid ‘portfolio greenwashing’.

- This paper introduces an attribution method, inspired by environmental economics, that enables the disentanglement of five drivers influencing portfolio emissions.

- To illustrate our model, we analyse a climate impact index and its benchmark over the period 2014-19. We show that the index reaches a similar decarbonisation rate to its benchmark by selecting the least emissions intensive companies within the sectors and companies that structurally reduce their emissions intensity.

- In contrast, the benchmark achieves this decarbonisation mainly through sector allocation.

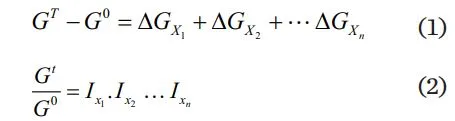

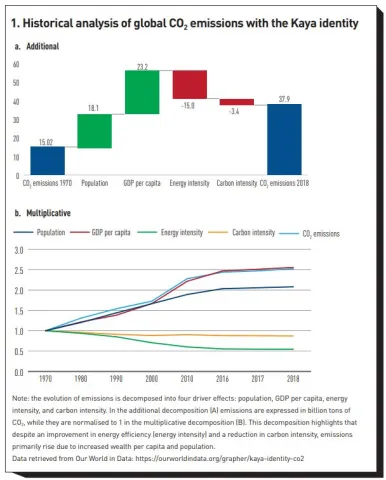

Investors are increasingly focused on managing greenhouse gas emissions in their portfolios to meet regulatory and stakeholder expectations. Despite existing climate metrics, investors face limitations in understanding and controlling the drivers influencing portfolio emissions. These challenges gave rise to initial attribution models inspired by financial Attribution analysis of greenhouse gas emissions associated with an equity portfolio Vincent Bouchet, ESG Director, Scientific Portfolio performance attribution models (NZAOA [2023]). Environmental economics research has faced similar issues and developed decomposition methods to understand different drivers of global emissions, such as the ‘Kaya identity’ (figure 1) that expresses global emissions as the product of population, GDP per capita, energy intensity and carbon intensity (Kaya [1990]).

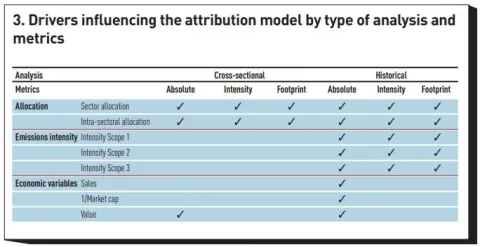

In a recent research paper (see Bouchet [2023] for more details), we propose a model for managing equity portfolio emissions inspired by decomposition methods from environmental economics. Our attribution model distinguishes five drivers applicable to metrics recommended by regulators and investor initiatives: sector allocation, intra-sectoral allocation, emissions intensity, sales and market capitalisation.

To illustrate our model, we analyse a climate impact index and its benchmark from 2014 to 2019. In cross-sectional analysis, the allocation within each sector driver explains nearly 70% of the difference in emissions intensity between the index and its benchmark, highlighting the index’s ability to be less emissions-intensive while minimising sector effects. In historical analysis, both the index and its benchmark experience a 35% reduction in emissions over the period. Notably, the climate impact index achieves decarbonisation primarily through intra-sectoral allocation and selecting stocks that reduce emissions intensity, whereas the benchmark relies on sector allocation, with less representation of high-emission sectors.

This framework enables investors to manage the degree to which emissions and their trends are influenced either by sector biases (potentially increasing risk with limited climate mitigation impact) or by selecting companies within sectors with lower and decreasing emissions. This qualitative perspective helps mitigate the risk of ‘portfolio greenwashing’, as defined by Amenc et al (2022).

The rest of the article is organised as follows. The second section introduces climate change expectations investors face and the need to understand drivers influencing portfolio emissions. The next section adapts a decomposition from environmental economics to equity portfolio emissions attribution analysis. The final section presents an analysis of a climate impact index and its benchmark.

Emissions metrics in finance

Climate metrics serve investors in meeting regulatory reporting demands, monitoring progress towards objectives and managing climate-related portfolio risks. This section covers current emissions metrics associated with a portfolio and forward-looking metrics projecting potential future emissions. Investor expectations initially focused on reporting but have shifted towards reduction targets. Therefore, investors must understand the drivers influencing portfolio emissions to meet these new expectations.

Current performance metrics

Current portfolio-level performance metrics are generally constructed by aggregating company-level metrics. This article only addresses emissions-related metrics. While there are additional metrics for monitoring climate impact and risks, emissions benefit from a mature accounting system and share a common unit.

At the company level, the Greenhouse Gas Protocol is the main framework for accounting and reporting. A central parameter is the emission scope under consideration, with Scope 1 accounting for direct emissions in production, Scope 2 for indirect emissions from purchased energy consumption, and Scope 3 for other indirect emissions along the value chain. The specific scope selection depends on the intended purpose of the metric. For emissions summation, using only Scope 1 is recommended to avoid double counting. For assessing a company’s global warming impact, a wider scope may be relevant. The distribution of emissions across scopes varies by sector. For example, the utilities sector predominantly features Scope 1 emissions, while the consumer staples sector has a majority in Scope 3.

The portfolio-level aggregation of performance metrics assumes company comparisons are acceptable. At the company level, comparability is typically achieved by normalising absolute emissions based on activity size or the company itself. The three commonly used denominators for normalisation – ‘sales’, ‘enterprise value including cash’ and ‘market capitalisation’ – each have pros and cons (Ducoulombier and Liu [2021]). At the portfolio level, the resulting aggregate metric represents the average of these intensities or footprints, weighted by company share in the portfolio. Considering the assets under management also allows the absolute emissions to be calculated (PCAF [2022]).

Forward-looking metrics

To address the limited insights that existing metrics provide relative to specific climate scenarios, forward-looking metrics have been developed to assess a portfolio’s alignment with the temperature change objectives of the Paris Agreement and other climate scenarios. ILB (2020) identifies four common steps to construct such metrics: 1) measuring portfolio-level climate performance, 2) selecting one or multiple scenarios, 3) converting macro emissions trajectories to portfolio trajectories, and 4) comparing the results of steps 1 and 3.

ILB (2020) highlights a wide disparity of results from different methodologies. For example, the implied temperature rise (ITR) of the Euronext Low-Carbon 100 index ranges from 1.5 to 3°C, depending on the methodology. These disparities limit the metrics’ effectiveness in conveying a portfolio’s alignment and monitoring portfolio emissions. Principles for Responsible Investment recommends that ITR metrics should be assessed alongside a range of additional climate metrics, including emissions (PRI [2021, 2022]).

From reporting to target-setting and monitoring emissions

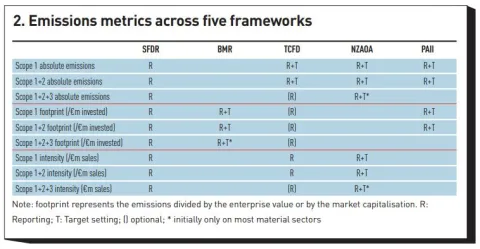

Expectations for investors are moving from current and past portfolio performance towards future objectives. Since the Paris Agreement, various frameworks have emerged to guide and organise investor practices related to climate change reporting, target setting and monitoring. This subsection examines emissions metrics used by the following frameworks (figure 2):

Regulatory frameworks:

- Sustainable Finance Disclosure Regulation (SFDR)

- EU Climate Transition and ParisAligned Benchmarks Delegated Regulation (BMR)

Institutional investor coalitions:

- Target Setting Protocol of the Net-Zero Asset Owner Alliance (NZAOA)

- Net-Zero Investment Framework by the Paris Aligned Investment Initiative (PAII)

Mixed framework (developed as a voluntary initiative, but increasingly mandated by regulators):

- Task Force on Climate-Related Financial Disclosure (TCFD)

Analysis of these frameworks highlights three points. First, the emphasis on reporting has evolved, with the frameworks now placing greater importance on target setting. Second, several initiatives require absolute emissions targets. Third, including asset-level Scope 3 emissions is becoming increasingly mandatory in reporting and target setting.

The attribution model we propose is designed to assist investors in meeting evolving expectations for emissions management (NZAOA [2023]). By analysing drivers that account for changes in a portfolio’s relative or absolute emissions, including asset-level Scope 3, the model serves several purposes. It facilitates an understanding of each driver’s role in reducing a portfolio’s emissions – beyond relying on sector allocation – which is particularly useful for assessing a portfolio’s potential to achieve reduction targets. It also provides inputs for shareholder engagement and transparency for public reporting (NZAOA [2023]).

An attribution method for portfolio emissions

In this section, we propose an attribution model to analyse different emissions performance metrics of an equity portfolio, from a cross-sectional and historical perspective, based on decomposition principles developed in environmental economics.

Theoretical principles of the index decomposition analysis

Various works in environmental economics identify the drivers of observed changes on environmental variables. This sub-section introduces index decomposition analysis (IDA) as it is the most easily applicable method for a financial portfolio.1

Consider G as an aggregate value of sub-categories h (eg, the sum of emissions associated with different instruments), and n drivers contributing to these sub-categories’ emissions x1, x2, ..., xn (eg, weight in portfolio, carbon intensity, sales, etc).

The goal of IDA is to understand historical aggregate change from G0 to GT as an (1) additive or (2) multiplicative operation between drivers.

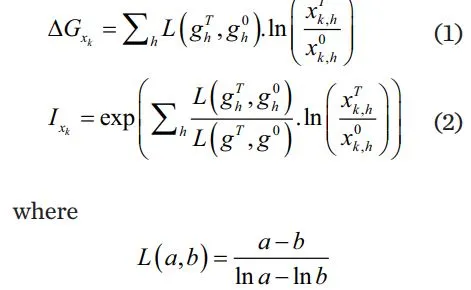

The reasoning behind the IDA is to derive the aggregate value formula over time and isolate the contribution of the n drivers. As developed in Ang (2015), the additional effects of the kth driver is given by

and gh is in our case the emissions of the instrument h.

The choice between additive and multiplicative methods depends on the analysis’ focus, with additive decomposition preferred for multi-year aggregate analysis and multiplicative decomposition preferred for identifying changes in trends.

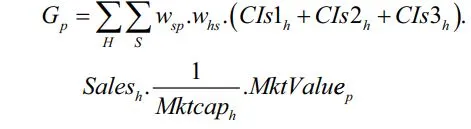

Identity for portfolio emissions

We present the identity for absolute emissions below.

The drivers can be grouped into three categories:

- Investment portfolio reallocation. The manager has a direct impact on sector and intra-sectoral allocation. The control of the sector allocation driver is particularly important and can be seen as an artifice relative to climate impact, allowing reduction of emissions by reducing exposure to emissive sectors. Sectoral deviations from a benchmark can cause large tracking errors, increasing financial risk.

- Emissions intensity (real world emissions reduction). Companies can lower their emissions intensity in three scopes (1, 2 and 3). Choosing companies that improve intensity is influenced by portfolio reallocation decisions. Throughout the article, Scope 1 + 2 emissions rely on reported data, while Scope 3 emissions are consistently estimated. This choice is driven by the lack of comparability in Scope 3 reported emissions and the goal of providing historical analysis.

- Economic drivers. These drivers link relative emissions and absolute emissions. Increasingly, frameworks recommend absolute emissions target-setting and monitoring. It is therefore essential to analyse absolute emissions and understand the economic drivers that influence them.

Sales – a company’s absolute emissions might be explained from a change in its emissions intensity or its sales.

– the share of emissions attributed to an investor depends on the market value of a company (for a fixed amount invested in this company).

– as the market value of a portfolio increases, the investor’s responsibility in terms of emissions increases.

Cross-sectional and historical analysis

Equity portfolio analysis can be historical or cross-sectional, such as against a benchmark. Depending on this choice and the type of metric analysed, only some drivers will influence the attribution model (figure 3).

Results

We illustrate the attribution model by comparing two portfolios: a conventional index of the US equity universe (500 stocks – the ‘benchmark’) and a climate impact index2 built on the same universe (the ‘index’).

Cross-sectional analysis

A portfolio’s cross-sectional analysis will only be influenced by sector allocation and intra-sectoral allocation. Figure 4a shows the drivers explaining the difference between the absolute emissions of the benchmark (left) and the climate impact index (right). The climate impact index’s lower decarbonisation can be explained by its lower exposure to high emitting sectors. However, the intrasectoral allocation shows that, even with similar exposure to these sectors, the index would have lower emissions because it is less exposed to the most emissions intensive companies. Sector and intra-sectoral allocation have a relatively similar effect when considering absolute emissions.

However, the weight of the two drivers in explaining the cross-sectional decarbonisation of the index depends on the metric considered. When analysing emissions intensity instead of absolute emissions, the results are different: the intra-sectoral allocation driver explains nearly 70% of the decarbonisation (figure 4b). The choice of metric for setting and monitoring targets is crucial, affecting the explanation of decarbonisation.

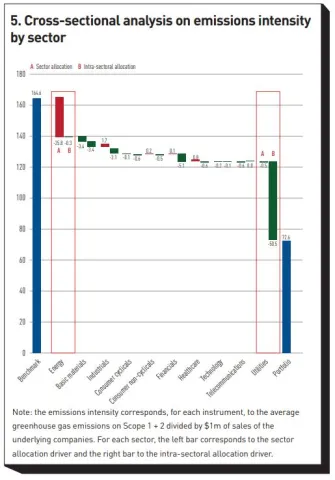

We want to identify sectors influencing these drivers, determining which sectors are over/underweighted by the climate impact index compared to the benchmark. The rearranged attribution model, presented in figure 5, examines these effects.

This analysis shows that the crosssectional difference is mainly explained by the energy and utilities sectors, although the drivers differ for each sector. Within the energy sector, the main effect is the sector allocation (left bar), while for the utilities sector, it is the intra-sectoral allocation (left bar). These results allow confirmation that the index provider has taken into account the exclusion criteria of the EU Benchmarks regulation and that they selected the ‘best in class’ within the other emissions-intensive sectors, in particular the utilities sector.

Historical analysis

The preceding analysis explains the difference between the climate impact index’s emissions performance and its benchmark’s performance at a given time. However, targets for decarbonisation objectives must be set over time. It is therefore essential to complement the cross-sectional analysis by a historical analysis.

This analysis introduces new drivers, including company emissions intensity (Scope 1, 2, and 3), sales and market capitalisation, reflecting the decarbonisation ‘trend’ of companies over time.

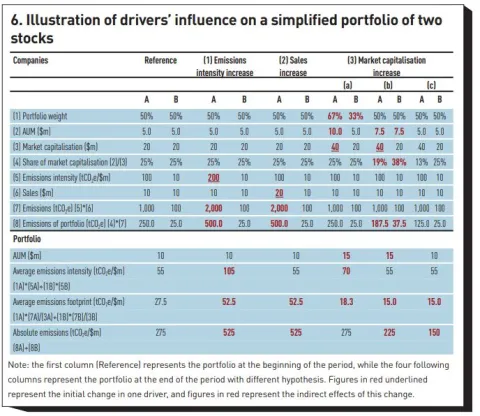

When examining absolute emissions, economic drivers (sales and market capitalisation) must be considered. A simplified example involving a portfolio with two equally weighted stocks illustrates how changes in emissions intensity, sales, and market capitalisation influence portfolio performance metrics – refer to figure 6, columns (1), (2) and (3) (a), (b) (c).

- If the market capitalisation of company A doubles, the average emissions intensity will increase because of the larger weight in company A, which is more intensive. Meanwhile, the footprint of the portfolio will decrease because absolute emissions are constant while the portfolio AUM is larger.

- With a hypothesis of an equally weighted portfolio, the AUM should be redistributed in the two companies. Such a change has no impact on the average intensity but has an impact on footprint and absolute emissions. Although the AUM is now 50% higher than in the initial state, the absolute emissions of the portfolio have decreased.

- The effect is amplified if we simulate an outflow of AUM.

This example illustrates the importance of considering several metrics to analyse a portfolio and the effects of economic drivers. The market capitalisation driver is difficult for a portfolio manager to control but has important short-term effects, so neutralising it when comparing the emissions performance of different instruments is relevant.

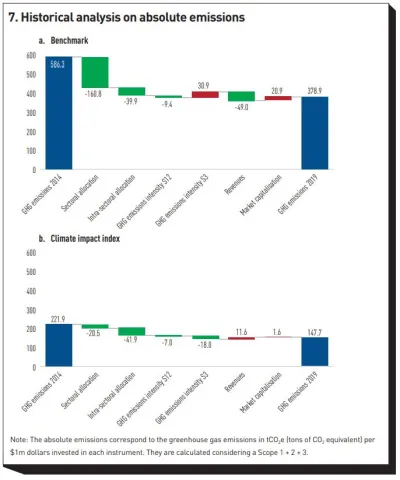

Figure 7a shows that most of the benchmark’s historical decarbonisation during the 2014-19 period comes from sector allocation. The emissions intensity driver contributes positively to the absolute emissions (on Scope 1 + 2 + 3). The main driver contributing to the climate impact index’s historical reduction is the intra-sectoral allocation (figure 7b). The emissions intensity driver also contributed to reducing emissions, while the sales driver increased them. This analysis shows how two similar decarbonisation rates can be achieved through different drivers.

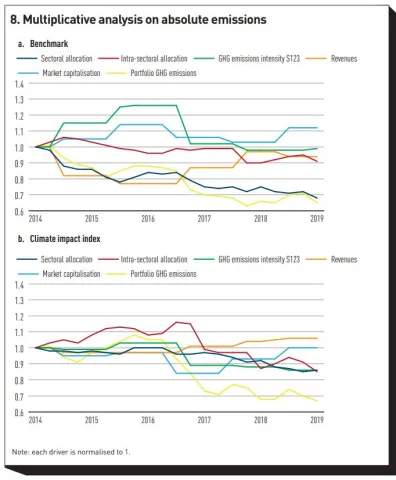

Using a multiplicative decomposition method provides insight into the historical trends of each driver. For the benchmark, sector and intra-sectoral allocation intensity, sales, and market capitalisation show more volatility (figure 8a). Additionally, although the index, on average, decarbonised similarly to its benchmark, it experienced an emissions increase from 2014 to 2016 (figure 8b). This multiplicative decomposition aids portfolio management by monitoring the evolution of drivers over shorter time periods.

Conclusion

In response to growing expectations of regulators and stakeholders for investors to manage the greenhouse gas emissions associated with their portfolios, we introduce an attribution analysis framework inspired by environment economics, allowing for both cross-sectional and historical analysis.

The proposed model parses the impact of three types of drivers: i) portfolio manager’s choices, ii) company emissions intensity and iii) economic drivers affecting total emissions. We illustrate this model by examining a climate-focused index and its benchmark. Despite both achieving similar decarbonisation rates, the climate impact index primarily reduces emissions through intra-sectoral allocation and lowering companies’ emissions intensity, while the benchmark achieves this mainly through sector allocation. Understanding each driver’s role helps verify if a portfolio effectively reduces emissions, preventing reliance solely on sector allocation and avoiding the risk of ‘portfolio greenwashing’.

This attribution analysis complements existing forward-looking approaches. While metrics like implied temperature rise are useful for communication, they have limitations in managing portfolio emissions (PRI [2021]). It’s crucial to distinguish methods for setting long-term alignment targets from those assessing and monitoring these targets. The attribution analysis framework in this article aligns with this assessment goal, emphasising the need for predefined portfolio-level targets compatible with global emission pathways.

From a practitioner perspective, it is possible to create a single metric to gauge a portfolio manager’s decarbonisation effectiveness. This metric can emphasise the manager’s skill in selecting top-performing stocks within sectors and ability to choose companies with decreasing emissions intensity. The metric can also eliminate the sector effect, preventing it from being perceived as ‘portfolio greenwashing’, as well as neutralising effects beyond the portfolio manager’s control.

Footnotes

- The structural decomposition analysis, the other main method, relies on the same mathematical principles but adds the input-output analytical framework developed by Wassily Leontief to the approach.

- Scientific Beta’s United States Climate Impact Consistent EU PAB Compliant index.

References

- Amenc, N., F. Goltz and V. Liu (2022). Doing Good or Feeling Good? Detecting Greenwashing in Climate Investing. The Journal of Impact and ESG Investing 2(4): 57-68.

- Ang, B. W. (2015). LMDI decomposition approach: A guide for implementation. Energy Policy 86: 233-238.

- Ang, B. W., and N. Liu (2007). Handling zero values in the logarithmic mean Divisia index decomposition approach. Energy Policy 35(1): 238-246.

- Bouchet, V. (2023). Decomposition of Greenhouse Gas Emissions Associated with an Equity Portfolio. Scientific Portfolio Publications.

- Ducoulombier, F., and V. Liu (2021). Carbon Intensity Bumps on the Way to Net Zero. The Journal of Impact and ESG Investing 1(3): 59-73.

- ILB (2020). The Alignment Cookbook – A Technical Review of Methodologies Assessing a Portfolio’s Alignment with Low-carbon Trajectories or Temperature Goal.

- Institut Louis Bachelier. Kaya, Y. (1990). Impact of Carbon Dioxide Emission Control on GNP Growth: Interpretation of Proposed Scenarios. Paper presented to the IPCC Energy and Industry Subgroup, Response Strategies Working Group, Paris, France.

- NZAOA (2023). Understanding the Drivers of Investment Portfolio Decarbonisation. UNconvened Net-Zero Asset Owner Alliance.

- PCAF (2022). Financed Emissions. The Global GHG Accounting & Reporting Standard, 2nd edition. Partnership for Carbon Accounting Financials.

- PRI (2021). Forward Looking Climate Metrics. Discussion Paper, Principles for Responsible Investment.

- PRI (2022). An Introduction to Responsible Investment: Climate Metrics. Principles for Responsible Investment.