Are physical climate risks adequately priced in markets?

That question framed Session 2 of the Principles for Responsible Investment "Physical Risk Community of Practice" workshop series with a presentation on Assessing Physical Risks: Data, Models, and Market Implications.

This session examined three practical challenges for investors:

-

the shrinking availability of public climate data;

-

the limitations of backward-looking scenario analysis;

-

and whether, and to what extent, physical risks are reflected in asset prices, a politicised question in some markets that nonetheless calls for evidence-based dialogue.

The format comprised opening remarks by Laura Weeks, Senior Responsible Investment Manager at PRI (10 min), a fireside chat with EDHEC Business School Professor Riccardo Rebonato (30 min), open discussion (15 min), and closing reflections (5 min). Participation was aimed at asset owners, investment managers, and service providers globally.

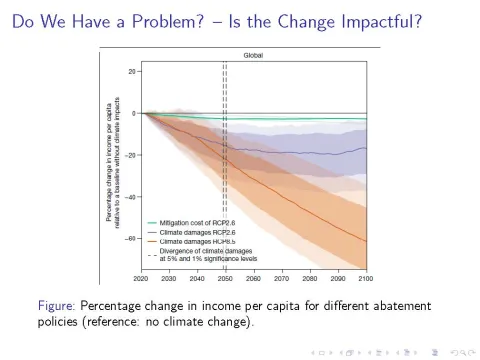

Professor Rebonato outlined the move from cataloguing visible damages to leveraging econometric evidence that links temperature to GDP primarily via productivity. The relationship is non-linear: output deteriorates slowly below an optimal temperature and more sharply above it. For investors, that translates into structurally lower cash-flow growth as the aggregate “pie” shrinks, with implications for equity and credit valuations over long horizons.

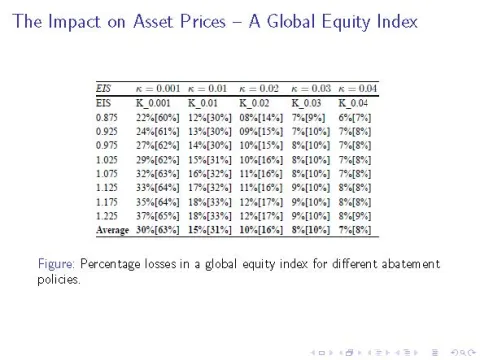

He observed that current market pricing appears incomplete. Evidence for a stable, priced “climate beta” in equities remains limited, and markets often struggle to incorporate low-probability, high-impact risks. This supports the view that climate damages, especially those tied to physical risk, tend to seep into earnings progressively, rather than being crystallised in a one-off repricing event.

On scenario design, he called for explicit probabilities and a rebalancing toward physical-risk pathways rather than reliance on transition-only narratives. As he put it:

“We have to do physical-risk scenarios as well… and we have to attach some probabilities to these scenarios. Unfortunately, the scenarios with the highest probability are the ones with the highest physical risk.” — Professor Riccardo Rebonato

Regarding the repricing path, he suggested that investors should plan for a sequence of negative earnings revisions—more of a grind than a cliff. Under slow-abatement pathways, he considered cumulative equity value impairment on the order of 30% to around 40% plausible over time, reflecting a smaller output base rather than a drawdown that mean-reverts.

The fireside Q&A concentrated on research depth and stewardship. The moderator captured the required scale with a clear message:

“When we talk about climate opportunities and investing in solutions… it’s basically an effort on a war-effort level.” — Kimberly Gladman, Senior Associate, Climate Change, PRI.

She emphasised issuer-level analysis of asset location, operational resilience and supply-chain exposure to physical hazards, with engagement practices that connect disclosures to capital-allocation decisions.

Further resources

White papers (by Riccardo Rebonato):

Articles (by Riccardo Rebonato):

EDHEC Climate research on physical risks (with Nicolas Schneider):